Transaction Center

Time to bring it home. Find zipForm®, transaction tools, and all the closing resources you'll need. Except for the champagne — that's on you.

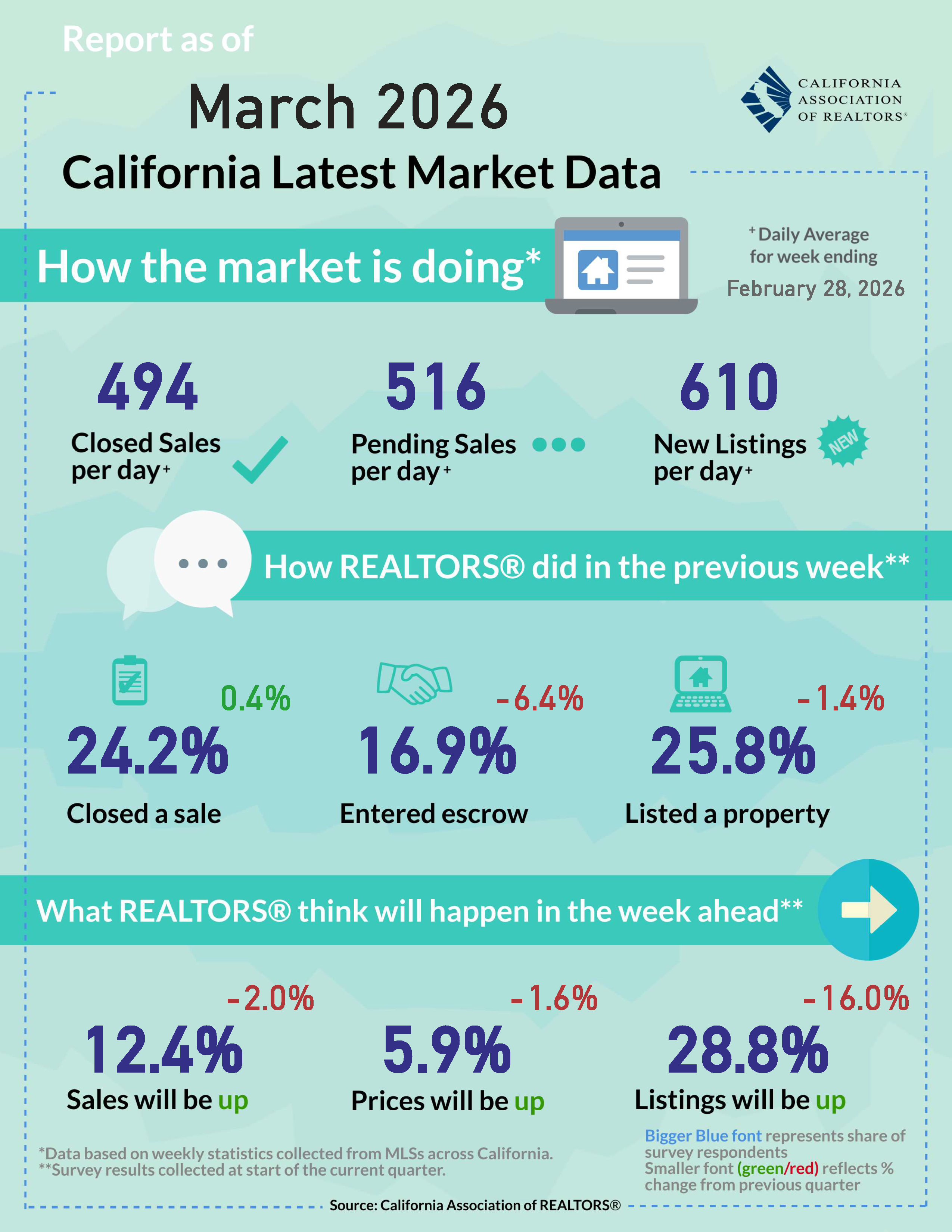

View the latest sales and price numbers. Find out where sales will be in upcoming months.

Get a roundup of weekly economic and market news that matters to real estate and your business.

Gain insights through interactive dashboards and downloadable infographic reports.

All Shareable Reports All Interactive DashboardsCatch up with the latest outreaches and webinars by the Research and Economics team.

C.A.R. conducts survey research with members and consumers on a regular basis to get a better understanding of the housing market and the real estate industry.

California Model MLS Rules, Issues Briefing Papers, and other articles and materials related to MLS policy.

Looking for information on how to file an interboard arbitration complaint? You've come to the right place! Find the rules, timeline and filing documents here.

Summaries and photos of California REALTORS® who violated the Code of Ethics and were disciplined with a fine, letter of reprimand, suspension, or expulsion.

The most recent edition of the Code of Ethics and Standards of Practice of the National Association of REALTORS® along with other important links to NAR information.

The California Professional Standards Reference Manual, Local Association Forms, NAR materials and other materials related to Code of Ethics enforcement and arbitration.

C.A.R. advocates for REALTOR® issues in Washington D.C., Sacramento and in city and county governments throughout California.

CREPAC, LCRC, IMPAC, ALF and the RAF comprise C.A.R.'s political fundraising arm.

The RAA: Protecting REALTORS® and Homeownership REALTOR® Action FundC.A.R. Senior Vice President Sanjay Wagle and former Senate Majority Leader Emeritus Robert Hertzberg discuss the Middle-Class Homeownership and Family Home Construction Act, a proposed ballot measure that seeks to address the growing barriers facing the next generation of would-be homeowners.

Learn how you can make a difference, by getting involved yourself or by passing along valuable information to your clients.

|

February 28, 2026 – Recent data suggest the economy and the housing market entered 2026 on firmer footing than headline growth at the end of last year might imply. Measures of sentiment improved in February, with both consumers and corporate leaders feeling more optimistic about the outlook, even as assessments of current conditions remain mixed. Households appear to be somewhat less concerned about future job prospects and incomes, while CEOs have become more confident about economic conditions over the next six months, despite ongoing cost pressures and policy uncertainty. In the housing sector, lower interest rates are beginning to provide incremental support, showing up in rising mortgage activity and early signs of stabilization in construction and new home sales. While affordability challenges persist, the balance of indicators points to gradual improvement rather than renewed deterioration. Consumer confidence edges up in February after a slow start in 2026: The U.S. Consumer Confidence Index improved slightly by 2.2 points in February from an upwardly revised 89.0 in January, according to the Conference Board. Despite the Present Situation Index remaining on a declining trend, the Expectations Index ticked up in the latest reading and pushed the overall index higher. Consumers were less negative about future business conditions and the labor market outlook in February and were more optimistic about their income prospects last month. Recent news on stronger job growth and more modest increase in inflation could have fueled the latest uptick in optimism. Respondents to the survey continued to believe interest rates to remain at higher levels over the next 12 months though, and most of them expected stock prices to be higher a year from now. Meanwhile, homebuying expectations were little changed in February from the prior month, but were above levels recorded a year ago. With rates back to their best rates in three years, homebuying optimism could improve in coming months as the market enters the traditional high season. CEO confidence jumps in Q1: Corporate leaders’ optimism also climbed up in the latest quarterly survey conducted by the Conference Board. In fact, the CEO Confidence Index rose sharply by 11 points to 59 in Q126 from 48 in Q425. Their six-month expectations for the economy flipped from slightly negative at the end of last year to moderate optimism in February 2026, as 43% of them said economic conditions should improve over the next six months, up from 24% in Q425. While the share of CEO’s who believed risks associated with trade and tariffs has dropped sharply to 32% in Q126 from 48% in Q425, more of them believed financial and economic risk could impact their industry as the share increased to 50% in Q126 from 44% in the prior quarter. More than two-thirds (71%) of the CEOs saw higher costs as a result of tariff increases, and 44% of them either have already passed on the costs to customers or plan to do so in the future. As such, upward inflationary pressure may still persist, and consumers could see higher prices in selected goods and/or services in the near term. Residential construction spending turns around at the yearend: U.S. construction spending bounced back in December with a 0.3% increase after falling 0.2% in November, the latest Commerce Department’s report shows. Total outlays were down 0.4% year-over-year from December 2024 and spending for the entire year of 2025 was 1.4% below the year-ago level. The modest month-over-month increase at the end of last year was attributed mostly to the increase in residential outlays, as new single-family in December climbed 1.5% from the prior month, while new multifamily inched up 0.1%. Meanwhile, private nonresidential spending dropped monthly in December and has been contracting for eight straight quarter, despite a surge in construction of data centers. With interest rates trending down in the past few weeks, building activity could pick up at the start of the year, and residential spending could see an improvement in 2026. New home sales show encouraging signs at the close of 2025: New home sales picked up at the end of last year, with transactions jumping 15.5% month-over-month in November but pulled back slightly by 1.7% in December. On a year-over-year basis, new home sales increased by 3.8% in December 2025 from 12 months ago. For the year as a whole, an estimated 679k new homes were sold in 2025, a dip of 1.1% from 686k units recorded in 2024. At the regional level, new home sales had the largest yearly increase in the Midwest (+30.1%) followed by the Northeast (+12.1%) and the West (+1.8%), while the South region (-1.1%) dropped slightly from the year-ago levels. The pickup in sales reduced housing inventory for the second straight month in December, with months of supply dropping down to a 7.6 month in December, the lowest level since July 2023. Lower rates and builders’ incentives continued to provide support to demand for newly constructed units at the end of last year and should lead to more new home sales in the next 12 months. Mortgage applications up as rates slide to lowest since 2022: Mortgage application volume was up slightly from the prior week for the week ending February 20, 2026, according to the latest weekly survey released by Mortgage Bankers Association (MBA). Mortgage applications on home purchases decreased 5% weekly on a seasonally adjusted basis, but the unadjusted figure was up 12% from a year ago. Refinanced applications were the primary driver for the overall increase, rising 4% week-over-week and surging 150% year-over-year. Rates sliding down to the lowest level in the past few years was the main contributing factor for the surge in applications. The pickup in mortgage applications in the latest MBA survey is an encouraging sign for the housing market and could provide early momentum heading into the spring homebuying season. Note: This summary report gets updated every Monday by 6:00 pm PST. Feel free to email us at [email protected] if you have any questions and/or feedback.

|

Quarterly Member Sentiment Report

|